It’s one of the big ironies in investing. You spend hours assessing a financial manager’s strategy and performance record, but neglect to ask about fees.

Then you wake up one day and realize that the 7% return on your carefully crafted portfolio is actually more like 5%.

Fees matter

The culprit? All manner of stated and hidden fees that you didn’t bother asking about.

Investing isn’t free. Investment products and services come with costs and fees.

They may seem trivial in isolation, but taken together these costs can take a big bite out of your nest egg over the long term.

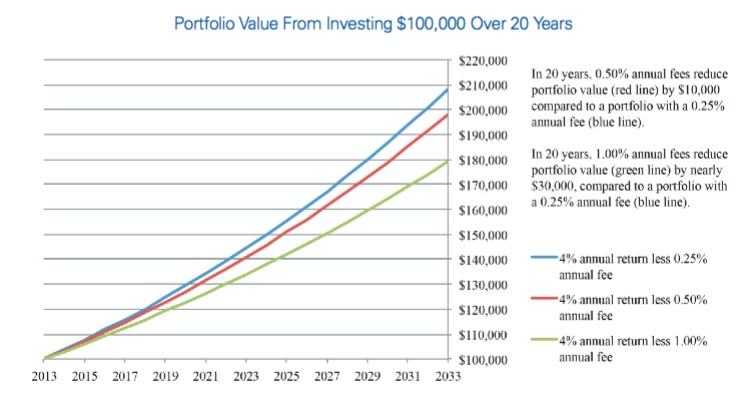

If you invested $100,000 and assumed 4% annual growth, your portfolio would take a $10,000 hit from a 0.50% annual fee and a $30,000 haircut if the fee burden was 1%, according to a recent SEC investment advisory.

So it pays to educate yourself about the sometimes opaque world of investment advisory fees.

Here’s how to bullet-proof your portfolio from excessive and well-hidden fees.

The basics

Broadly speaking, there are two broad categories of fees. Transactional fees reflect the cost to you of buying, settling or selling a security.

The second type of fees (usually calculated on an annual basis) reflect overhead and administrative costs to cover portfolio management, fund administration, fund accounting and pricing, shareholder services (such as call centers and websites), distribution charges, and so on.

Special care needs to be taken when assessing mutual fund commissions, also known as loads. There are front-end loads, back-end loads and ongoing loads.

Mutual funds can be useful investments in any portfolio, but do the math on commissions. You will need returns that exceed these costs before you make any money.

So much for the standard fees. From here, things can get pretty complicated in a hurry.

Hidden fees

Investors need to be on the hunt for fees that don’t show up in the marketing brochures and FAQ pages of websites.

For instance, some investment management firms charge investors fees to cover the cost of marketing and distributing the fund.

If you are paying a stock broker a commission, make sure you are actually getting the advice that the payments are meant to be funding.

Ask him to review your portfolio and come up with recommendations that add value.

If you no longer need that handholding that was required when you started out investing, there are other options out there.

There are plenty of online platforms with low fees that cater to “do-it-yourself” and semi-involved investors, ready to take greater control over their financial decisions, but that also offer personalized advice when needed.

Just be sure the solution you choose is upfront about fees, and you can understand how and when you’ll be charged.

Conflict of Interest

Investment brokers often have a web of business relationships with other firms that may not be in the best interest of their clients.

For instance, some financial firms pay independent investment advisers a commission for steering clients into their products.

That’s not necessarily a bad thing if the product is a sound one and the client understands the financial relationships behind the recommendation.

The partnership may have come out of a long-term respect for each other’s offerings, and results in still doing the best thing for the client (you.)

However, not all stock brokers disclose these background commissions and at the same time collect a management fee from their clients.

That’s called double dipping, and should raise a red flag about your broker’s integrity. Asking point blank, “What are all the ways you or your firm will make revenue off my choosing to invest with you?” is a tough question, but one that can save you thousands of dollars in the long-run.

Additionally, many financial advisors who are employed by a brokerage or financial firm have restrictions as to what they can offer you, usually centered around their employer’s offerings. It’s important to find out and understand what these restrictions might be for you and your wealth management team.

What to do?

Investors need to be vigilant and spend just as much time scrutinizing the fee structure of the investment as they do do calculating risk and potential return.

It requires a frank discussion with your investment adviser to make sure you’re getting straight answers about fees.

If you feel like you are getting the run around, consider checking out traditional brokers and online platforms that offer transparent descriptions of feeds and that present up-to-date returns on a post-fee basis. With so much information readily available, it’s easy to simply start with those who make these answers easy to find and just as easy to understand.

Though it can take a little effort, doing more thorough vetting up front can help you feel a sense of calm and trust as the years unfold.

Follow the money

Advisers can be compensated in many different ways, including a flat fee, hourly, as a percentage of assets, or by commissions on the investments they recommend.

Brokers and investment advisers that rely on commissions from third parties have a special burden to be open about where their revenue comes from. And if there are potential conflicts of interest, you deserve to be made aware of them.

Of course, financial professionals need to make a living and should get paid for their services. That said, investors deserve fully transparent descriptions of fees in a clear and understandable language.

If you are overpaying, don’t be afraid to negotiate a new rate or consider looking at alternative traditional and online options available to investors who want to keep fees to a minimum.

You may be surprised by how easy it is to lower your fees.

Think of it as an instant investment return.

DISCLAIMER: The information in this material is not intended to be personalized financial advice and should not be solely relied on for making financial decisions.

{kind=link}