The swoon in oil and natural gas prices has drawn a lot of unflattering attention to the energy industry. As it happens, two of my largest holdings in the Dividend Paying Large Caps portfolio are Ecopetrol (EC) and Lukoil (LUKOY).

In October, I actually increased my position in Ecopetrol, so the question is why?

Why are energy prices going down?

In my opinion, there are basically two major factors that are currently impacting the price of crude oil worldwide.

The first is the spread of Ebola in Western Africa and other parts of the world, and the second is that the US has overtaken Saudi Arabia as the biggest oil producer in the world.

Oil extraction from shale formations across the US in places like Texas, Pennsylvania, and North Dakota has caused a surge in supply, which combined with restrictions on exporting crude is curbing the price of West Texas Intermediate, America’s oil benchmark.

How low they can go?

I don’t think prices can go much lower for few reasons.

Hydraulic fracking drillers will be under considerable pressure and financial stress. These companies spent more money than they brought in during the boom, and they made up the gap by borrowing.

This was fine as long as the oil sold at a high price. When crude oil becomes inexpensive, margins decline and they won’t be able to get as much money for their product as they originally thought.

This industry is massive in the US and Canada, and putting them under pressure is not in the best interest of the US government. If crude oil prices continue to go down ($75 or less), companies that rely on fracking will have a hard time repaying their debt.

Economic impact

For many countries, the low price of oil directly translates into economic woes – including, most dramatically, the possibility of a contracting economy.

According to a recent article in Bloomberg Businessweek, if pricing remains under $104 a barrel, Russia will face a drop in its gross domestic product by up to 1.5 percent.

Prices are currently below $90. If an economy as big as Russia’s suffers, then other countries around the world will also feel the pain.

Annual investment in oil and gas across the country is at a record $200 billion, reaching 20 percent of the country’s total private fixed-structure spending for the first time.

If this industry gets hit too hard for too long, that will impact other market segments, and the US economy in general. Low prices are good, but prices too low for too long will not be good news for anybody.

If we look at historical prices of oil versus gas, we see that they move in tandem. Oil prices vs gas prices behave very similarly to stock prices vs earnings.

They can deviate from the mean once in a while, but at the end of the day, they will eventually always need to correct course.

If oil prices increase too quickly when compared with gas prices, there will always be a correction. That’s what happened in 2008, and that’s what is happening now.

Oil prices may go lower, but we are certainly near the bottom of this trend. I don’t think the current low prices will be sustainable for much longer

Energy rebound?

Now that the US is the biggest producer in the world, I don’t expect huge increases in oil or gas prices anytime soon.

Gas prices will rise as soon as the economy improves. Obviously, I don’t have crystal ball, but over time energy stocks may outperform other market segments. That said, we may still be a couple of years away from that moment.

In the meantime, you can collect dividends from most of these companies in my opinion.

So to answer the question, why did I increase my exposure in the energy sector?

I would say: Prices won’t go much lower than current levels because it is not good for the economy or for the fracking companies that the US government is trying to protect.

It is a big sector that if it hits a recession has the potential to drag the entire economy down.

These companies pay healthy dividends, in the order of 3% and above. So even if stock prices don’t go up for a while, I’ll be happy to wait a couple of years while collecting the dividends.

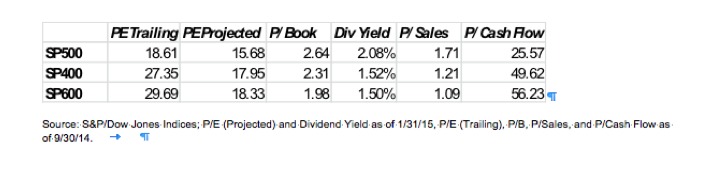

PE ratios are very low when compared with other segments of the market making this an excellent opportunity to take advantage of before the economy improves and prices start to rise.

Gainers

In October Apple (AAPL), American Express (AXP) and Bed, Bath & Beyond (BBBY) performed well.

Apple continues to have a good moment after releasing the new and very well received iPhone 6 and 6 Plus in September.

American Express is doing an excellent job targeting more diverse audiences, and is currently paying better dividends than MasterCard (MA) and Visa (V).

Bed, Bath & Beyond (BBBY) continues its recovery after the big drop that it faced this year from January to May. Although the company still down for the year -15.1%, since August the stock has increased 10.4%. Price to sales ratio is only 1.1 and the company has no debt.

Losers

In October, my worst performing stock was JC Penney (JCP), down -24%. Because of this single position, my portfolio underperformed the S&P 500 for the month.

After reaching $11 in August, the stock took a hit and is currently trading at $7.20. This stock is extremely undervalued at the moment in my opinion.

Price to Sales ratio is 0.1. Very low compared with the 7.2 of Macy’s (M). I’ll keep this holding in my portfolio, but I know that the recovery will take at least 1 year more.

Yearly revenues from the company are finally increasing, after deep declines in 2012-2013. I have no way of knowing for sure, but I expect this stock to have a very good 2015.

The other company that took a big hit in October was Ecopetrol. For the reasons mentioned above in this article, the whole energy sector is suffering lately.

I think this sector crisis is at the bottom and I also expect Ecopetrol to do very well in 2015, especially if the economy sees an improvement.

Acquisitions in October 2014

I added Adidas (ADDYY) to my portfolio, the stock has been down -45% this year, but this is a great company, with a global presence and very well diversified.

The stock has been dragged down by the European Stock market, which is not having a great year. Price to sales is 0.7, nothing when compared with the 2.9 of Nike (NKE). Adidas has not been this cheap in many years.

I also added Copa (CPA), a very interesting airline company operating in Latin America that was “unfairly” hit because of worldwide Ebola concerns. Many airlines have been down because of this, offering great entry point opportunities. I may consider selling it at some point.

The only position I liquidated in October was Wells Fargo (WFC). Great company that I had to sacrifice in order to take advantage of better opportunities on the stock market.

Photo Credit: Barta IV via Flickr Creative Commons

DISCLAIMER: The investments discussed are held in client accounts as of October 31, 2014. These investments may or may not be currently held in client accounts. Dividends reflect past performance and there is no guarantee they will continue to be paid. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Past performance is no guarantee of future results.