Successful investing requires a long-term view and a certain amount of discipline. That’s particularly true when it comes to the practice of portfolio rebalancing.

This refers to the habit of regularly buying or selling investments to make sure a portfolio sticks to the strategic asset allocation goals that sync with your financial goals and risk tolerance.

Left unmanaged, portfolios have a tendency to drift as a result of market moves. If you have some spectacularly winning investments, they can end up naturally representing a huge chunk of your portfolio. Your reasonable 60% (equities) and 40% (fixed income) portfolio can quickly become an 80% (equities) and 20% (fixed income) mix if an explosive bull market occurs.

The sensible thing to do is to trim back on those winning stocks and reallocate those gains into laggard investments to bring a portfolio back into balance with your original allocation goals. Taking gains on a white-hot investments isn’t an easy thing to do for some investors, but history shows it is the right move for the long haul.

Remember, no asset class soars forever. Financial stocks ruled in the mid-1990s, then technology stocks had their run toward the end of that decade. Both ran out of gas as did homebuilder stocks after the housing bubble in the middle of last decade. At some point the current five-year bull market is going to stumble as well.

That’s the beauty of rebalancing. Nobody has a crystal ball and can know which asset class, sector or investing style is going to boom or bust in 2015. Rebalancing helps you reap the full rewards of diversification. A well-balanced portfolio gives an investor a better chance of protecting gains and allowing one to benefit from a change in the market’s direction.

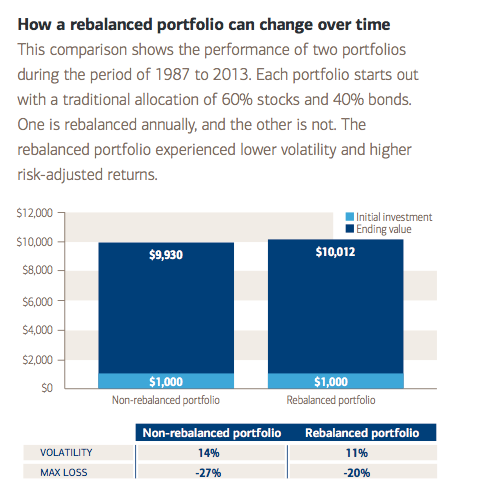

Take a look at this graphic from a May 2014 research report from Merrill Lynch comparing two portfolios (one rebalanced and the other not) from 1987 to 2013. The regularly balanced one experienced less volatility and higher risk-adjusted returns.

The trick is knowing when and how often to rebalance. After all, reshuffling the deck isn’t free. Capital gains taxes may be due upon the sale if the asset sold has appreciated in value, and don’t forget the transaction costs (brokerage commissions, purchase and redemption fees) to execute and process the trades for exchange traded funds or mutual funds. Finally, there is the time or labor costs that you or your investment manager take on to compute the rebalancing amount.

Some investors set up a regular rebalancing schedule (monthly, quarterly or annually) and then pull the trigger if their portfolio has drifted away from their allocation goals by a certain percentage, say 5%, 10% or 15%. Others act regardless of time if their threshold target has been breached.

Ideally, a well-diversified portfolio will have cash flow such as interest payments, realized capital gains, or new contributions. And these funds can be used to trim the costs of rebalancing. Sweeping taxable portfolio cash flows into a money market or checking account and then redirecting these flows to the most underweighted asset class as part of their scheduled rebalancing event is a cost efficient way to go.

So how often should one rebalance? Every investor has a different risk tolerance, so there is no golden rule. However, it probably makes sense to review your portfolio on a quarterly or semiannual basis. It might be time to rebalance if your allocations drift by 5% or 10%.

To learn more about Covestor, contact our Client Advisers at clientservices@interactiveadvisors.com or give them a shout at 1.866.825.3005. Or you can try Covestor’s services with a free trial account.

Disclaimer: All investments involve risk and various investment strategies will not always be profitable. No investment strategy, including asset allocation or diversification, can guarantee a profit or protect against a loss. Past performance does not guarantee future results.

{kind=link}