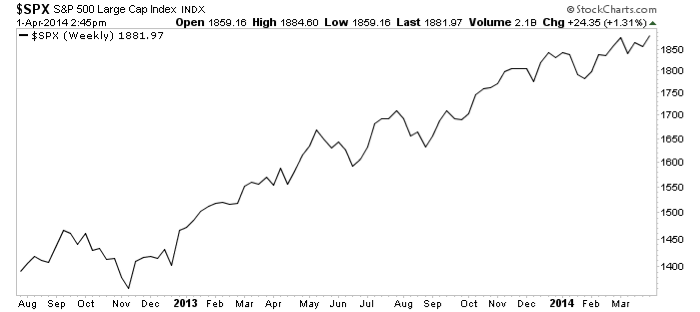

The bull lives. This year has gotten off to a rocky start due to a combination of lackluster American economic data and, more significantly, emerging market volatility. But after bottoming in early February, the S&P 500 Index (SPX) has clawed back to its all-time highs.

Emerging markets equities have rebounded as well; the iShares Emerging Markets ETF (EEM) has roughly tracked the S&P 500 after bottoming out in early February. European shares, measured by the iShares Europe ETF (IEV) continue to outperform both U.S. and emerging market equities.

Through February 28, my Tactical ETF portfolio is pacing the S&P 500. The aggressive allocation to mortgage REITs has been one of the the best-performing portfolio position, followed by our allocation to Spanish equities.

The gains have been roughly neutralized by weak performance in Chinese stocks, where the portfolio is overweight. I continue to expect Chinese equities to outperform this year, but they are getting off to a slow start, along with most emerging market indices.

My Dividend Growth portfolio is off to a solid start this year, up 4.4% vs. 1.0% for the S&P 500 through February 28. As bond yields have moderated, yield-sensitive investments have enjoyed a nice rebound.

In a prolonged period of lower-than-usual market yields, I expect the Dividend Growth’s strategy of combining a high current yield with expected growth in the dividend payout to be a strong performer. Within this sphere, I see the best values among conservative retail and industrial REITs, and I expect this subsector to be a major focus throughout 2014, market conditions warranting.

I also made one significant change to my Strategic Growth Allocation. I reduced my allocation to the Vanguard Dividend Appreciation ETF (VIG) and added a new allocation to the Cambria Shareholder Yield ETF (SYLD).

While I am still a big believer in VIG’s long-term strategy of investing in companies with a history of raising their dividend payouts, I consider SYLD’s approach of combining dividend growth with share repurchases to be a worthwhile enhancement.

I seldom make changes to the Strategic Growth Allocation, as it is designed to be a passive “buy and hold” allocation. But I consider SYLD’s approach to be an enhancement that was significant enough to warrant a portfolio shakeup.

Meanwhile, I continue to maintain an overall bullish stance. Consistent with my comments of recent months, I intend to maintain an overweighted allocation to income and emerging market stocks and to European stocks.

DISCLAIMER: The investments discussed are held in client accounts as of February 28, 2013. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable. Past performance is no guarantee of future results.

{kind=link}