News that Japan’s third-quarter GDP slowed to 1.9% has certainly given some ammunition to investors who believe Japan’s economy is losing momentum at best—or is careening toward a debt and currency crisis at worst.

Over the past year, Japanese Prime Minister Shinzo Abe has had some success reviving the world’s third biggest economy with a mix of fiscal stimulus, radical monetary expansion and tax incentives to boost business. The policies, known as Abenomics, have triggered an explosive rally in the Nikkei, which is up 45% as of November 14, 2013.

However, there are two big challenges facing Japan. First off, the fiscal easing and the Bank of Japan’s bond buying program haven’t been followed up with industry deregulatory reforms Abe has promised to secure long-term growth.

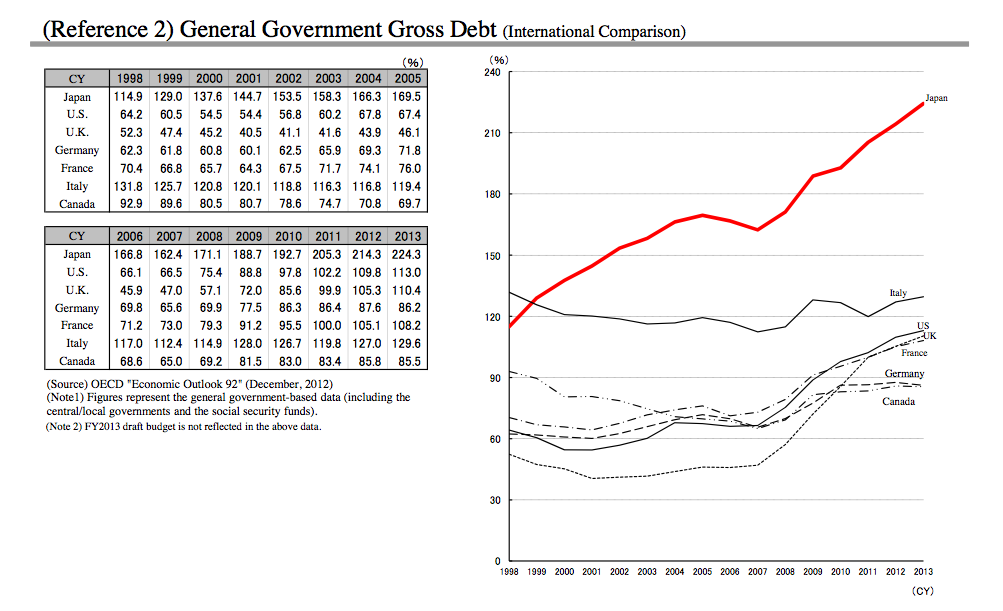

Secondly, Abe is hemmed in by Japan’s gargantuan debt burden, the highest in the developed world. The International Monetary Fund sees Japan’s government debt reaching 310% of its GDP by 2030 if Abenomics don’t deliver on promised economic reforms to increase trade and open up more protected businesses to global competition.

Abe’s government has decided to raise the country’s consumption tax to 8% from 5% currently. The prime minister wants Japan to achieve a primary budget balance—in which government revenue equals outlays, excluding debt-service costs on existing liabilities—by 2020.

Daiwa Institute of Research analyst Mikio Mizobata estimates the consumption tax actually needs to be more like 19% if the government is serious about hitting that goal, given rapidly expanding outlays for social security and the state-run healthcare system.

Hedge fund manager J. Kyle Bass, whose Hayman Advisors made $500 million during the U.S. subprime crisis, predicts a Japanese fiscal collapse and has shorted Japanese bonds. In his view, Japan’s debt burden is so large that at some point investors are going to start dumping bonds and that will place upward pressure on Japanese bond yields and government debt-service costs.

Covestor portfolio manager Charles Sizemore is also bearish about Japan’s economic prospects. Here’s his case in a nutshell:

More than half of all Japanese government spending is financed by new borrowing. This means that half of every yen borrowed is used to service existing debts. It’s a debtor’s nightmare that gets worse every year with budget deficits that are consistently higher than 7% of GDP. All of this might be manageable if Japan were a young and growing country. But it’s not, and it never will be again (or at least not in our lifetimes). Japan is the oldest country in the world, a place that sells more adult diapers than infant diapers. It’s population — and tax base — is shrinking, and its national savings rate — once among the highest in the world — is now lower than that of the United States.

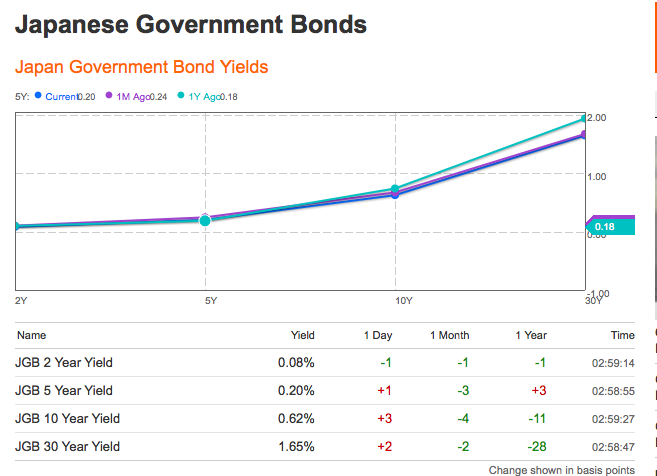

Yet the Japanese government bond market shows no signs of stress at the moment. Ten-year yields on Japanese government bonds are hovering around 0.62% as of November 15, one of the lowest levels in the world.

Nor does demand for Japanese bonds seem to be lagging. On November 14, an auction of 2.45 trillion yen ($25 billion) worth of five-year bonds was oversubscribed by a factor of five.

However, if Japan doesn’t start growing more robustly in 2014 and its debt burden continues to climb, the tranquil bond market could get turbulent in a hurry.

What gives Japan bears confidence are the huge fiscal and demographics challenges ahead. Already, there is huge pressure on Japan’s government budget to finance its current debt and spend on social programs, given the country’s aging population.

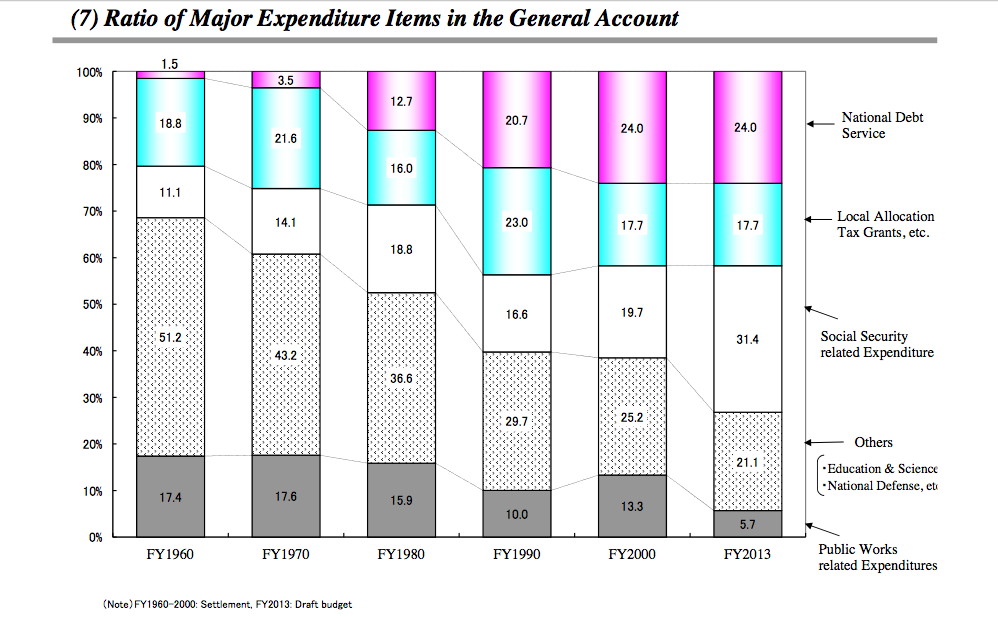

Looking at the country’s major budget expenditures, Japan is spending about 24% on debt service and 31.4% on social security related programs.

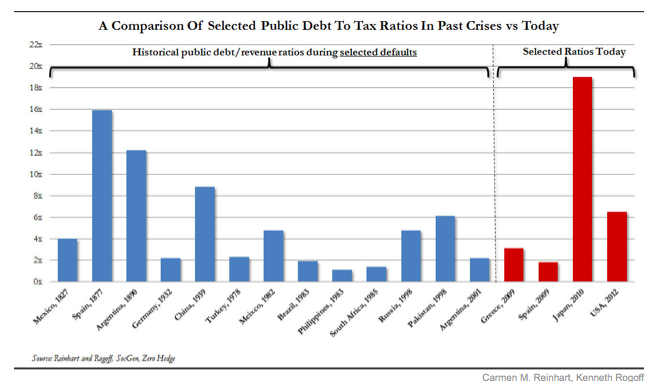

Japan has been running trade deficits over the last 15 months and that raises concerns about the sustainability of its high government debt level. By one measure, debt relative to tax revenues, Japan is truly in a class of its own.

Photo Credit: arcreyes [-ratamahatta-]

DISCLAIMER: All opinions included in this material are as of November 15, 2013 and are subject to change. Foreign investments may be volatile and involve additional risks including currency fluctuations, and political and economic uncertainties. The information in this material is not intended to be personalized financial advice and should not be solely relied on for making financial decisions. Past performance is no guarantee of future results.

{kind=link}