Let’s start with a look at a few important macro charts.

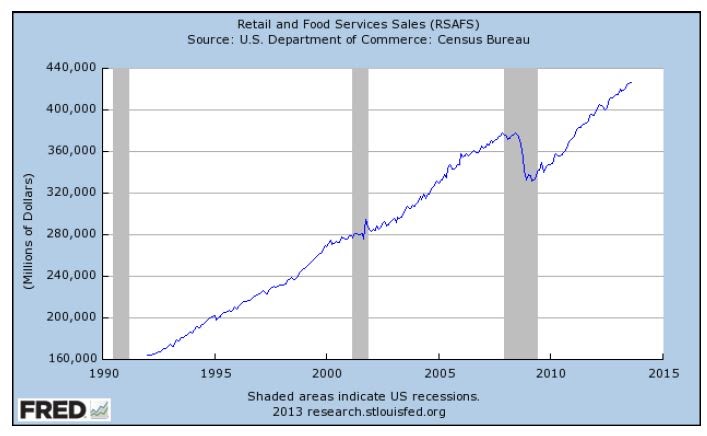

Retail sales appear to be maintaining a nice growth trend:

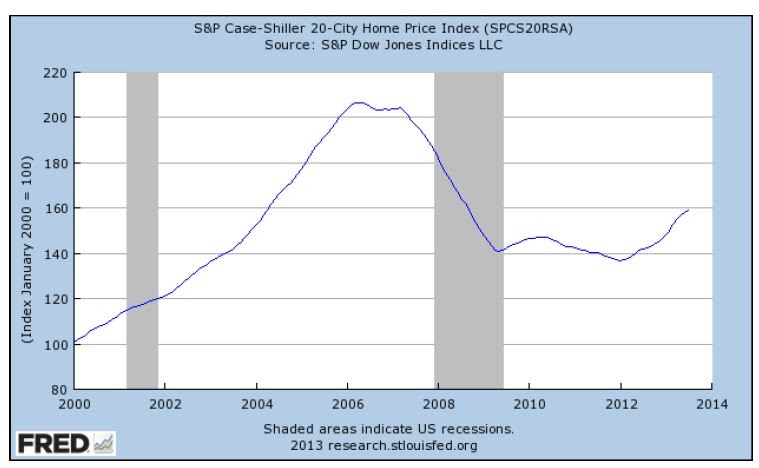

Home prices – Better, but still well under the bubble conditions that preceded the meltdown.

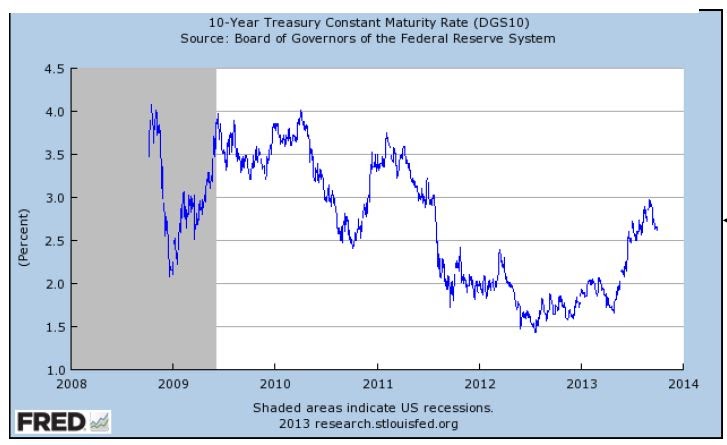

10-Year Treasury – You can see the sizeable climb in the yield of long-term Treasuries after the Fed announced it was strongly considering a reduction in its bond buying program (aka taper) in May. You can also see the rate dip at the end when the Fed surprisingly announced in September that they would not taper at that time:

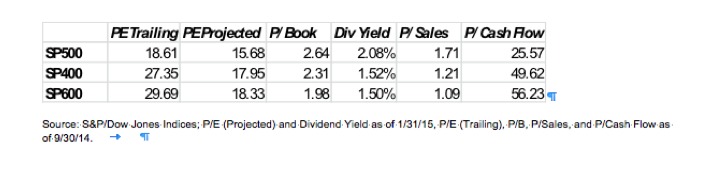

Data: St. Louis Federal Reserve, Standard & Poors, Frank Russell, MSCI

With all that is going on in government, I thought the following quotes and comedic relief from Will Rogers offer a nice way to start:

“There’s no trick to being a humorist when you have the whole government working for you.”

“We have the best congress money can buy.”

“Politics is applesauce.”

“Be thankful we’re not getting all the government we’re paying for.”

“The more you read and observe about this politics thing, you got to admit that each party is worse than the other.”

The big news in the quarter was the Fed’s September decision to not taper activity in their $85 billion monthly bond buying program. Despite setting some strong expectations, the Fed ultimately felt that the economy was not strong enough to produce sustainable growth without assistance.

This was a big surprise to many, including myself. Another surprise in the announcement was the Fed’s concern over looming spending authorizations and debt limits in need of approval by congress and the President. Venturing into political waters is a unique development for the Fed.

To the Fed’s credit, they were right to be concerned as we are currently under a partial government shutdown at the time of this writing. A standoff has developed around spending and healthcare reform. This is concerning but so was the meltdown of Europe about a year or two ago.

In my opinion, this economic problem is probably not as big as either Europe or the headlines the press gives this issue. As for eventual legislation, I believe pressure and fear will force politicians to make decisions to restore government before any significant consequences develop.

This has been a fairly consistent outcome during previous periods of political contention. While it does not seem to matter much right now, the Fed may have paid itself an unexpected favor with its taper decision that is keeping it out of controversial world of politics.

As for the real economy, seasonal strength that often comes with late summer and early fall did not come to bear this year. This outlook was probably the basis of the Fed’s spring expectation that a cutback in bond buying would be appropriate around September.

Employment, industrial production, inflation and employment numbers are only sending signals of modest strength and growth. There is also concern that higher long-term rates may be affecting real estate sales. With all that is going on in politics and the economy, it also seems very unlikely that the Fed would make a move in October.

A move is made even more difficult by the fact the partial shutdown has turned off the flow of economic numbers that form the basis of many Fed decisions. An unstable Middle East and the likely appointment of a new Fed chairman remain important items as well.

Looking ahead for stocks, current market valuations and earnings expectations point to a fairly valued market right now. A longer term outlook, however, is encouraging with the Fed being careful and sensitive to signals of weakness.

Furthermore, many company managers continue to effectively execute operating and capital strategies in their businesses. There are also signs of improvement in Europe and the developing energy story in the United States has strong implications for the future. For the fixed income markets, I believe long-term rates remain unattractive even though yields are notably higher than a year ago.

The investments discussed are held in client accounts as of September 30, 2013. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable.