Despite very troubling conditions, equity markets in the third quarter of 2012 produced meaningful and broad gains. With gains like this, one would expect to hear that corporate earnings were up or that the economy has improved. Neither was the case, as earnings estimates fell and the economy remained on a sluggish growth trend. What appears to be the basis for the strong equity performance in the latter part of the quarter were the actions and words of global central bankers.

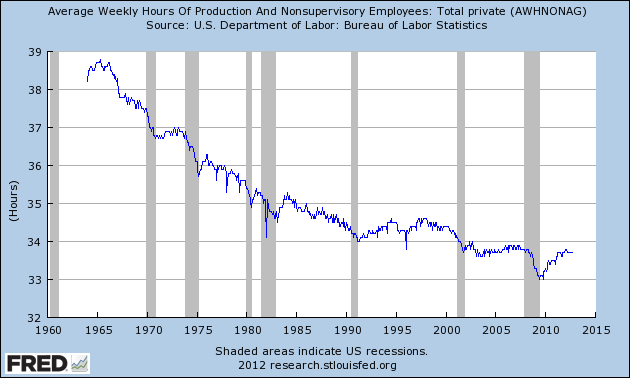

AVERAGE WORKWEEK HOURS – This is a potential leading indicator assuming companies will ask current workers to work more hours before hiring additional workers. Right now, this indicator is not pointing to meaningful job growth:

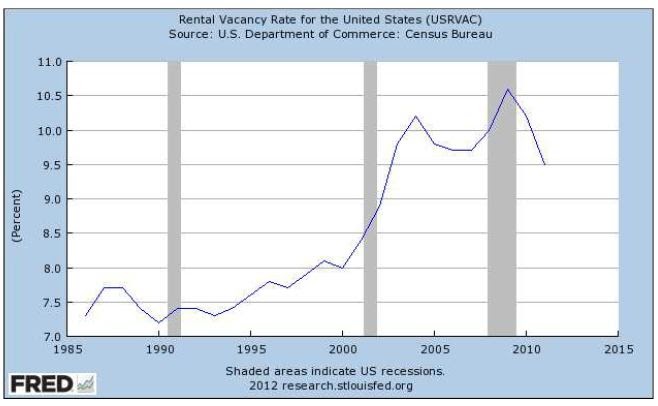

RENTAL VACANCY RATES appear to be falling sharply. This should drive rents higher and ultimately lead to further improvement in the housing market:

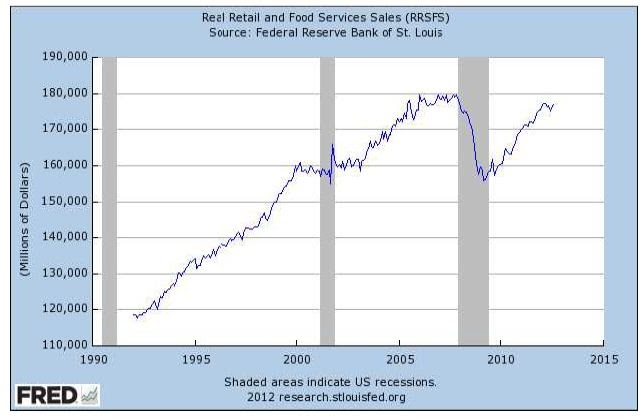

It is nice to see RETAIL SALES nearly back to pre-crisis levels:

Data: St. Louis Federal Reserve

In Europe, central bankers were talking about buying the debt of troubled countries that commit to strong austerity measures. While such talk has been going on for a while, they appear to be getting more serious and appear to be advancing in the decision process. Here in the United States, the Federal Reserve announced a third and a very aggressive round of quantitative easing (printing money), greater twist (sell short-term securities and buy long-term securities to lower long-term rates), and an extension of the commitment to maintain short-term rates at very low levels through 2015.

At the same time equity investors enjoyed “central banker” benefits, bond investors did not see much benefit as long-term rates did not fall a great deal during the quarter. The 10-year Treasury constant, a measure of 10-year US Treasury rates, only fell from 1.67% to 1.65%. However, bond prices did advance in the previous quarter with a rate decline from 2.23% to the mentioned 1.67%.

To their credit, the bond markets appear to have accurately anticipated Federal Reserve policy moves. Given their recent stability, interest rates appear to be in balance (albeit at low and unattractive return levels) with the policies and outlook advertised by the Fed.

Equity market valuations, with a forward price to earnings ratio around 14x, appear to be at a level with reasonable return potential even with the recent advance and estimate declines.

While on the subject of expectations, it would be remiss to ignore politics. Currently, very few people think Congress can get anything done and the upcoming “fiscal cliff” has potential to become reality.

Perhaps the markets are expressing their worry with strong fund flows into fixed income securities. The advance of the equity markets, however, strongly suggest that the “Fiscal Cliff” issue will get addressed in some shape and form after the election. I also believe this is the likely scenario. As for the Presidential election, some have suggested that certain stocks are implying an Obama win. I don’t think there has been anything decisive in market movements to suggest such an outlook.

In closing, it looks like the Fed is the strong player right now and it appears that it wants to stay that way until job creation reaches a sustainable level. This may take some time. Despite the troubled nature of the current investing environment, the Fed’s support and general investor feelings of risk aversion provide basic underpinnings for worthwhile long-term equity returns. I also think it is highly likely that it will be a bumpy ride given the variety of volatile global conditions we currently face.

Many thanks for your business and interest in Timberline.

Certain of the information contained in this presentation is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. Covestor believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.

{kind=link}